Need Professional Advisor ?

Need Professional Advisor ?

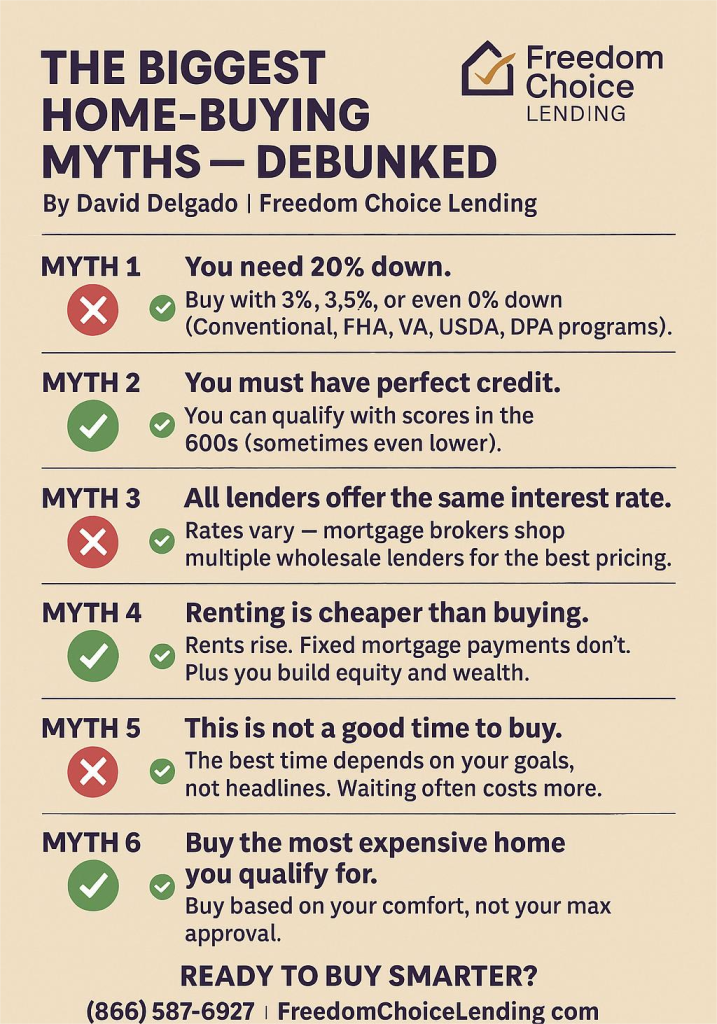

By David Delgado | Freedom Choice Lending

For many first-time buyers, the biggest challenge isn’t the housing market…it’s the misinformation surrounding it.

Every day, I talk to renters who are ready to buy but feel held back by myths they’ve heard from friends, family members, or social media. These misconceptions can delay your journey to homeownership — or even stop you altogether.

Let’s clear the air. Here are the most common myths about buying a home…and the truth that can finally move you forward.

Myth #1: “You need a 20% down payment.”

Truth: Many buyers purchase with 3%, 3.5%, or even 0% down.

The 20% rule is one of the biggest misunderstandings in real estate. In reality:

- Conventional loans allow as little as 3% down.

- FHA loans require just 3.5% down.

- VA and USDA loans allow 0% down for qualifying buyers.

- Down-payment assistance may cover some or all of your upfront costs.

For many of my clients, the real barrier isn’t cash — it’s clarity. Once we break down the numbers, they realize homeownership is much closer than they thought.

Myth #2: “You need perfect credit to qualify.”

Truth: You can buy a home with a credit score in the 600s — and sometimes even lower.

Perfect credit is not required. Loan programs are flexible:

- FHA loans allow scores as low as 580 (and sometimes 500 with compensating factors).

- Conventional loans offer competitive options with mid-600 scores.

- I help clients create a credit improvement strategy when needed to boost scores quickly and strategically.

Your credit score affects your rate — not your ability to explore your options.

Myth #3: “All lenders offer the same interest rate.”

Truth: Rates vary significantly — and a mortgage broker saves you money.

Many buyers assume rates are standardized. Not true.

As a mortgage broker with Freedom Choice Lending, I compare wholesale lenders — including large institutions like UWM — to find the most competitive pricing available.

This means:

- Lower rates

- Lower fees

- More loan program options

- Faster closings

You’re not locked into one bank’s rate sheet. You have choices.

Myth #4: “Renting is cheaper than buying.”

Truth: Rent rises every year. Fixed mortgage payments do not.

Even when market conditions shift, buying often builds wealth faster than renting.

Here’s why:

- Rent increases, but fixed mortgage payments stay the same.

- A portion of every mortgage payment goes toward your principal, not your landlord’s pocket.

- Homeowners benefit from equity growth, tax advantages, and long-term stability.

If you plan to stay in an area for 3+ years, buying often becomes the more affordable path.

Myth #5: “This isn’t a good time to buy.”

Truth: The best time to buy depends on your goals — not headlines.

Yes, interest rates move. Yes, markets shift.

But waiting for the “perfect” moment often leads to one result: higher prices later.

Real estate has historically appreciated over time. Even modest appreciation can create tens of thousands of dollars in equity in just a few years.

The right time to buy is when you:

- Have stable income

- Understand your budget

- Want long-term financial growth

- Are ready to invest in yourself instead of paying rent

Your personal strategy matters more than market noise.

Myth #6: “You should always buy the most expensive home you qualify for.”

Truth: Buy based on comfort — not maximum approval.

A lender approval is a guideline. Your budget is personal.

I walk every client through a clear analysis:

- Your lifestyle

- Your savings and future goals

- Your true monthly comfort level

Buying a home should empower you — not stretch you.

Myth #7: “You can’t buy a home if you’re self-employed.

Truth: Self-employed buyers have many loan options, including bank-statement and alternative-income programs.

Whether you’re a business owner, contractor, or freelancer, lenders have solutions tailored to your income structure.

We use:

- 12- or 24-month bank statements

- Profit-and-loss evaluations

- Asset-based programs

- Expanded approval options

If you’ve been told “no” before, it might simply mean you didn’t have the right lender.

The Bottom Line: The Path to Homeownership Is Closer Than You Thin

Most home-buying fears come from misinformation — not reality.

If you’re thinking about buying a home this year, the smartest move you can make is a real conversation with a mortgage professional who will break things down clearly and honestly.

Let’s go over your numbers, discuss your goals, and create a plan that fits your life.

Direct Line (562) 281-6163

Main Office (866) 587-6927

David Delgado – NMLS #349079

Presiden/CEO

Freedom Choice Lending

NMLS #1998153

Click Here To Schedule a 15 Loan Consultation Call

Fast Approvals call (562) 281-6163

No Money Down Payment Programs

Reverse Mortgages

FHA

Jumbo

Conventional Elite (Easy to qualify)

97% Conventional Financing

Bank Statements, P&L Only , No Income No Tax Returns

Shop Your Loan With Over 200 Loan Products From The TOP Wholesale Lenders In The Country!

On Time Closings Guaranteed or We Will Pay $1000 penalty fee!*

**Be aware! Online banking fraud is on the rise. If you receive an email containing WIRE TRANSFER INSTRUCTIONS call your escrow officer immediately to verify the information prior to sending funds.**

Leave a Reply