Need Professional Advisor ?

Need Professional Advisor ?

If you’re currently renting and thinking about buying a home, your credit score is one of the biggest factors standing between you and approval.

The good news: getting to a 620 FICO score—the minimum for many loan programs like FHA and conventional financing—is very achievable with the right strategy.

This isn’t about waiting years. With the right moves, you can build or repair your credit in a matter of months.

Why 620 Matters

A 620 FICO score is the threshold where financing options open up:

- FHA loans (low down payment options)

- Conventional loans (depending on scenario)

- Better interest rates vs. sub-600 scores

- Lower overall monthly payments

Below 620, your options shrink. Above 620, you gain leverage.

Step 1: Open the Right Type of Credit Card

If you don’t have active credit—or your score is low—the fastest way to build is with a secured credit card.

These cards are designed for credit building:

- You put down a small deposit ($200–$300)

- That becomes your credit limit

- The bank reports your payments to all 3 credit bureaus

Strong Starter Options

- Capital One (Platinum Secured)

- Discover (Discover it® Secured)

- OpenSky (Visa Secured – no credit check)

- Chime (Credit Builder Card)

These companies specialize in helping clients establish or rebuild credit quickly.

Step 2: Use Credit Like a Lender Wants to See

This is where most people either build their score fast—or stay stuck.

Follow these rules:

- Keep your balance under 30% of your limit (ideally under 10%)

- Use the card for small, consistent purchases (gas, groceries)

- Pay on time every month—no exceptions

Why this matters:

- Payment history = 35% of your score

- Credit utilization = 30% of your score

This is over half your score—controlled by just these two behaviors.

Step 3: Add a Second Account (Accelerate Growth)

After 2–3 months of on-time payments:

- Open a second secured card OR

- Become an authorized user on a family member’s credit card

This improves:

- Total available credit

- Credit depth

- Overall profile strength

More importantly, it speeds up your path to 620.

Step 4: Avoid These Credit Killers

If your goal is speed and approval, these are non-negotiable:

- No late payments (this can drop your score fast)

- Don’t max out your cards

- Avoid applying for multiple accounts at once

- Don’t close accounts once opened

Consistency beats everything.

Step 5: Realistic Timeline to 620

If you follow this system correctly:

- 30–60 days: Score begins to generate or improve

- 90–120 days: Noticeable increase

- 4–6 months: Enter the 580–600 range

- 6–9 months: Reach 620+

This is the difference between continuing to rent… and owning a home.

The Bigger Picture: This Is About Approval, Not Just Score

Getting to 620 isn’t just a number—it’s about showing lenders that you’re predictable, consistent, and low risk.

You don’t need:

- Perfect credit

- High income

- Large down payment

You need a repeatable system that proves you can manage debt responsibly.

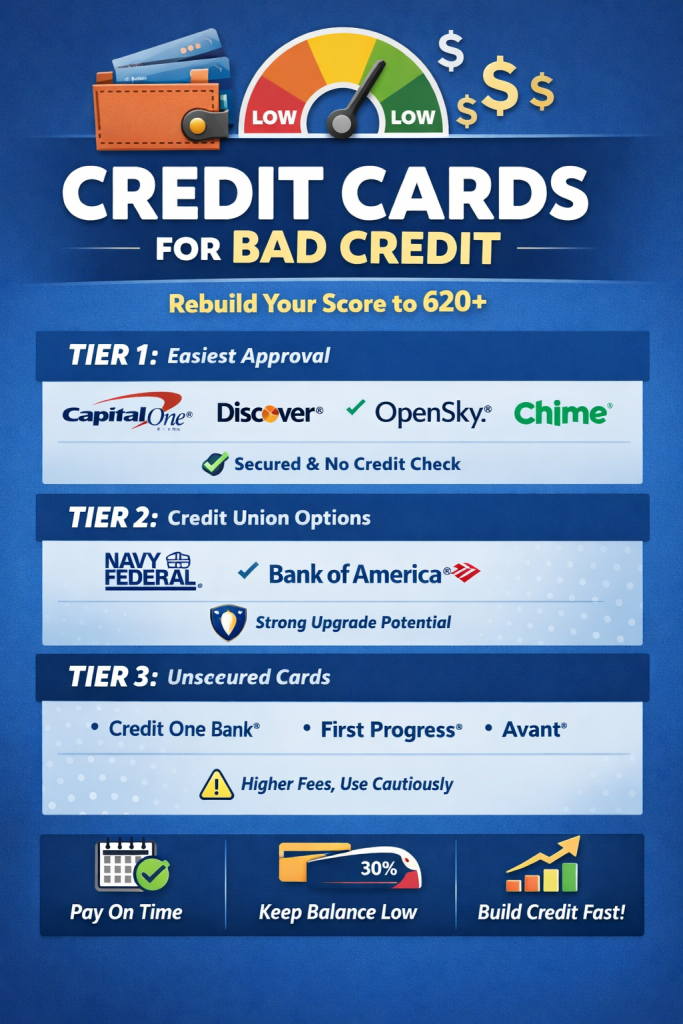

Credit Card Companies That Work With Bad Credit

Tier 1: Highest Approval Odds (Best Starting Point)

These are secured or no-credit-check options—your fastest path to getting approved and building toward a 620.

- Capital One

- Strong for low credit profiles

- Offers pre-approval (no hard inquiry upfront)

- Low deposit options

👉 https://www.capitalone.com/credit-cards/platinum-secured/

- Discover

- One of the best for rebuilding credit

- Cashback + potential upgrade to unsecured

👉 https://www.discover.com/credit-cards/secured/

- OpenSky

- No credit check required

- Ideal if score is very low or recent issues

👉 https://www.openskycc.com/

- Chime

- No credit check

- Works like a debit/credit hybrid

👉 https://www.chime.com/credit-builder/

📌 Why these work: Secured cards require a deposit, reducing lender risk—making them much easier to approve for bad credit borrowers

Tier 2: Credit Union & Bank Secured Cards (Underrated Advantage)

These are powerful but often overlooked—especially for long-term growth.

- Navy Federal Credit Union

- Very flexible underwriting

- Strong upgrade path to high limits

👉 https://www.navyfederal.org/

- Bank of America (Secured Cards)

- Reports to all bureaus

- Solid for transitioning to unsecured

👉 https://www.bankofamerica.com/credit-cards/

- DCU

- Lower interest rates vs competitors

👉 https://www.dcu.org/

- Lower interest rates vs competitors

📌 Strategy: If you can get into a credit union, approval odds and long-term limits improve significantly.

Tier 3: Easier Unsecured Options (Use Carefully)

These don’t require a deposit—but approval is harder and fees can be higher.

- Credit One Bank

- First Progress

- Avant

📌 Reality check:

Unsecured cards for bad credit exist, but they often come with higher fees and stricter terms, so secured cards are usually the better starting point

How to Choose (Execution Strategy)

If your goal is fastest path to 620, don’t overthink it:

Best path (highest ROI):

- Start with:

- Capital One OR Discover

- If denied → go to:

- First Progress – Avant – OpenSky or Chime (guaranteed entry-level)

- After 60–90 days:

- Add a second card

- Add a second card

What Actually Moves Your Score (This Is What Matters)

- Pay 100% on time (non-negotiable)

- Keep balance under 10–30%

- Let accounts age (3–6 months minimum)

- 📌 Secured cards are specifically designed to help rebuild credit because they report to all three bureaus and reward consistent payment behavior

Bottom Line

You don’t need perfect credit—you need access + consistency.

The right 1–2 accounts from the list above, used correctly, can realistically get someone to:

- 580 → ~600 in 3–4 months

- 600 → 620+ in 6–9 months

Final Thought

Most renters think they’re years away from buying.

In reality, many are just one or two credit accounts and a few months of discipline away from qualifying.

If you’re serious about buying, start now. Every month you delay is another month of missed equity and rising home prices.

Want a Custom Plan?

If you want a personalized strategy based on your current credit profile and timeline, I can map out exactly what you need to do to hit a 620 and position you for approval.

The sooner you start, the faster you’re holding keys.

Leave a Reply