Need Professional Advisor ?

Need Professional Advisor ?

Claremont, CA, known for its tree-lined streets and prestigious colleges, remains a desirable place to live. But with home prices hovering around $1.2 million, many are wondering: should I buy or rent? Let’s break down a real-world comparison using current market data, including an interest rate of 6.25% and 95% conventional financing.

The Scenario

- Purchase Price: $1,200,000

- Down Payment (5%): $60,000

- Loan Amount: $1,140,000

- Interest Rate: 6.25%

- APR: 6.397%

- Loan Term: 30 years fixed

- Forecasted Home Appreciation: 5.54% annually

- Estimated Rent for Comparable Property: $4,200/month

- Annual Rent Increase: 4%

Key Questions We’ll Explore

- How does rent paid over time compare to equity built through homeownership?

- What kind of wealth can buyers expect to build through appreciation and principal repayment?

- When does buying start to financially outperform renting?

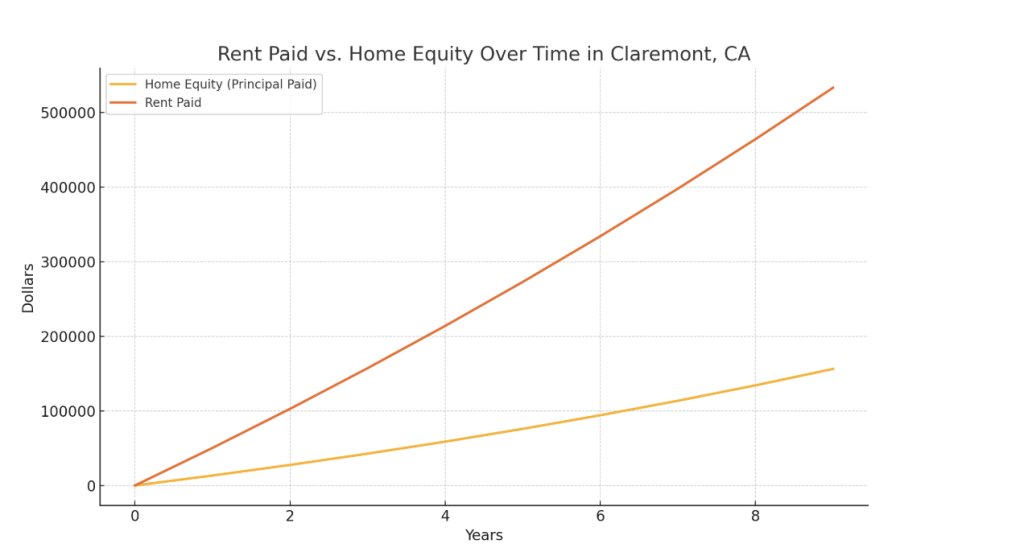

Chart: Rent Paid vs. Home Equity Over 9 Years

Below is a chart comparing cumulative rent payments with equity (principal) accumulated by a buyer over a 9-year period:

Observations:

- By Year 3: Renters will have paid nearly $155,000 in rent, while buyers will have built up more than $80,000 in equity.

- By Year 6: Rent payments approach $337,000, while home equity exceeds $180,000.

- By Year 9: Buyers surpass $300,000 in principal equity, while renters will have spent over $540,000 on housing with no return.

Beyond Principal: The Power of Appreciation

In addition to paying down the mortgage, Claremont homes are expected to appreciate at 5.54% annually. Here’s what that looks like:

| Year | Home Value | Total Appreciation |

|---|---|---|

| 0 | $1,200,000 | – |

| 3 | $1,408,635 | $208,635 |

| 6 | $1,652,278 | $452,278 |

| 9 | $1,938,179 | $738,179 |

Combined with principal paid, total owner equity by year 9 exceeds $1,000,000 in wealth building.

Cost Considerations

Monthly Housing Payments:

| Item | Buyer (Est.) | Renter |

|---|---|---|

| Mortgage (P&I) | $7,022 | $4,200 |

| Property Taxes | ~$1,250 | — |

| Home Insurance | ~$150 | — |

| PMI | ~$450 | — |

| Total | ~$8,872 | $4,200 |

While monthly ownership costs are significantly higher upfront, equity and appreciation ultimately tip the scale in favor of buying—especially for those planning to stay for 5+ years.

The Bottom Line

Buying Wins in the Long Run If:

- You stay at least 5–7 years.

- You want to build long-term wealth through appreciation and loan paydown.

- You have the resources to cover a higher monthly payment and closing costs.

Renting May Make Sense If:

- You’re unsure about your long-term plans.

- You want lower monthly payments and minimal maintenance responsibility.

- You prefer liquidity over tying up funds in real estate.

Final Thoughts

While buying a $1.2M home in Claremont requires a serious financial commitment, the long-term benefits—especially in a high-appreciation market—are hard to ignore. Renters pay for housing with no return, while homeowners grow their net worth year after year. If you’re planning to plant roots, buying may be the smart move.

David Delgado – NMLS #349079

President/CEO

Main Office (866) 587-6927

Freedom Choice Lending

NMLS #1998153